I had a friend in college who moved to Zambia almost right after graduation. A young, single female she showed a lot more courage than those of us who thought we were tough guys, but only talked about being adventurous.

She worked for a few years with improving the Zambian health care system. Occasionally she shared anecdotes about life in that southern African country. One curiosity was that the TV news stations suspended weather forecasts for a few months every year. Asking a co-worker, she was told that “we all know the sun will shine until rain season comes”.

Here in the United States we cannot afford that luxury. We depend on our weather forecasters, and they are wrong, we blame their inaccurate forecast for the fact that it rained during our family camping weekend.

As an economist I have great sympathy for meteorologists. Believe it or not, in my profession forecasting is tougher. Now, for example, I predict that we are a year, maybe 18 months, away from a new recession. I do so based on national accounts data and data from the labor market; there is some support for my forecast on the global stock markets. Yet one of the nation’s most reputable economics research institutions, the Congressional Budget Office, has an entirely different view of the economy.

In their latest outlook the CBO predicts that GDP will continue to grow at 2.1-2.2 percent per year from 2018 through 2025, without even a hint of a recession in the future. In fact, the CBO actually predicts an increase in growth in 2016-17.

So here we are, me vs. the CBO. Who is right? It should be the CBO, should it not? After all, they have infinitely more resources at their disposal than I do.

Not so fast. While economic forecasting is notoriously difficult, there are two basic rules that help getting it right. First, know your economics. Standard macroeconomic theory explains why business cycles come and go. It says that there will never be long periods of uninterrupted growth unless exceptional circumstances are present.

Secondly, a good economic forecast relies on history, and history tells us that we usually do not have more than four years, five at the most, between recessions. The U.S. economy is now four years out of a recession. For this reason alone it is a good idea to be on the lookout for signs of the next downturn.

These two basic rules, together with careful analysis of macroeconomic data lead me to predict a mild recession starting in the second half of 2016.

Does this mean that I think the CBO is wrong? No. They are more focused on predicting effects of long-term trends in the economy than to predict short-term fluctuations. At the same time, as economists we always have to keep in mind how our work is used. It is well known that Congress relies heavily on CBO outlooks when making fiscal policy decisions.

For this reason CBO could be a bit more cautious about future business cycle swings than they are in their ten-year outlooks. For example, their latest outlook could be interpreted as saying that Congress has plenty of time ahead to address the budget deficit – after all, it will not reach $1 trillion again until 2025.

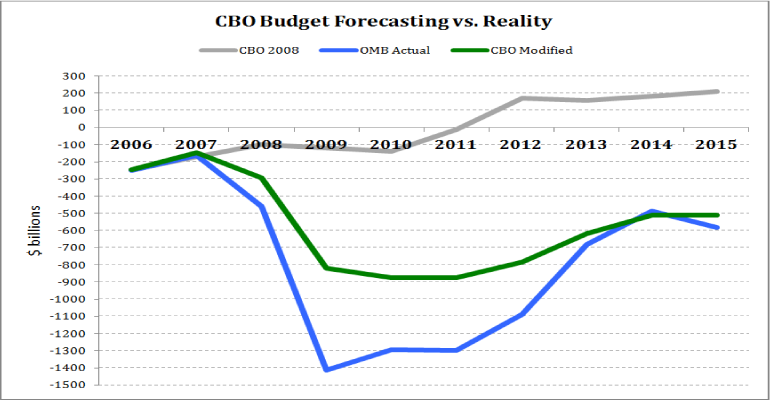

The problem is that if I am correct about the next recession the budget deficit will reach $1 trillion and more within the next 2-3 years. To put the difference between my forecast and the CBO outlook in perspective, let us go back to the budget forecast for 2008 that the CBO published in 2007. As shown by the grey function in the figure below, the CBO predicted the budget deficit would gradually vanish and turn into a surplus in 2012.

In reality, starting in 2008 the deficit exploded, as illustrated by the blue function. Part of that had to do with dramatic, yet temporary increases in federal spending under the American Recovery and Reinvestment Act. But even if CBO had been pinpoint accurate about federal spending, the recession would have created massive deficits because tax revenue plummeted (the green line):

Sources: Congressional Budget Office; Office of Management and Budget.

Sources: Congressional Budget Office; Office of Management and Budget.

The point here is not to bash the CBO. They are a fine institution with many good, hard-working economists. The point is instead to highlight the dire nature of forecasting, and the incredible responsibility that comes with advising legislators. What if the CBO had predicted the Great Recession in 2007 – a recession that began a year later – along, say, the green line? Is it possible that Congress and then-President Bush would have taken pre-emptive measures already in 2008? Could that have prevented the recession from becoming as bad as it did?

It remains to be seen who is correct about 2016. I hope the CBO will be correct, but I fear that I will be. If I am correct, it is not inconceivable that we could see a repetition of Figure 1, with a rapidly growing, “unexpected” deficit. Given where we are right now, with a government debt larger than GDP, weak growth and interest rates trending upward, that would be a bad place for Congress to find themselves.

I will leave it to our elected officials whom they should listen to.

Sven Larson, Ph.D., is an economist and Member of the Council of Scholars of Compact for America. He is the author of Industrial Poverty (Gower Publishing) about the debt crisis in Europe. Find his daily blog articles at America’s Fiscal Future.